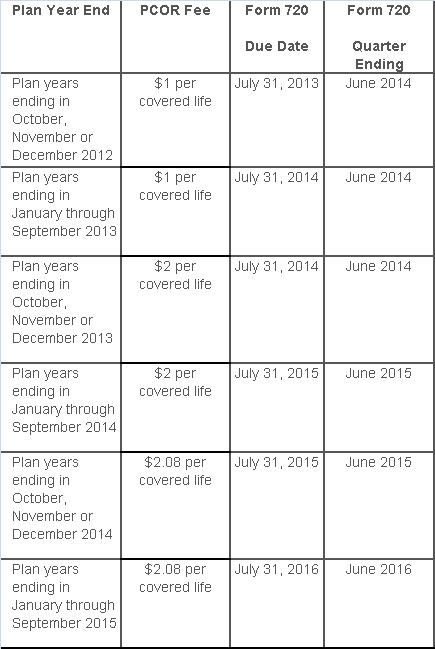

The Affordable Care Act added a patient-centered outcomes research (PCOR) fee on health plans to support clinical effectiveness research. The PCOR fee applies to plan years ending on or after Oct. 1, 2012, and before Oct. 1, 2019. The PCOR fee is due by July 31 of the calendar year following the close of the plan year. For plan years ending in 2014, the fee is due by July 31, 2015.

PCOR fees are required to be reported annually on Form 720, Quarterly Federal Excise Tax Return, for the second quarter of the calendar year. The due date of the return is July 31. Plan sponsors and insurers subject to PCOR fees but not other types of excise taxes should file Form 720 only for the second quarter, and no filings are needed for the other quarters. The PCOR fee can be paid electronically or mailed to the IRS with the Form 720 using a Form 720-V payment voucher for the second quarter. According to the IRS, the fee is tax-deductible as a business expense.

The PCOR fee is assessed based on the number of employees, spouses and dependents that are covered by the plan. The fee is $1 per covered life for plan years ending before Oct. 1, 2013, and $2 per covered life thereafter, subject to adjustment by the government. For plan years ending between Oct. 1, 2014, and Sept. 30, 2015, the fee is $2.08. The Form 720 instructions are expected to be updated soon to reflect this increased fee.

This chart summarizes the fee schedule based on the plan year end and shows the Form 720 due date. It also contains the quarter ending date that should be reported on the first page of the Form 720 (month and year only per IRS instructions). The plan year end date is not reported on the Form 720.

For insured plans, the insurance company is responsible for filing Form 720 and paying the PCOR fee. Therefore, employers with only fully- insured health plans have no filing requirement.

If an employer sponsors a self-insured health plan, the employer must file Form 720 and pay the PCOR fee. For self-insured plans with multiple employers, the named plan sponsor is generally required to file Form 720. A self-insured health plan is any plan providing accident or health coverage if any portion of such coverage is provided other than through an insurance policy.

Since the fee is a tax assessed against the plan sponsor and not the plan, most funded plans subject to ERISA must not pay the fee using plan assets since doing so would be considered a prohibited transaction by the U.S. Department of Labor (DOL). The DOL has provided some limited exceptions to this rule for plans with multiple employers if the plan sponsor exists solely for the purpose of sponsoring and administering the plan and has no source of funding independent of plan assets.

Plans sponsored by all types of employers, including tax-exempt organizations and governmental entities, are subject to the PCOR fee. Most health plans, including major medical plans, prescription drug plans and retiree-only plans, are subject to the PCOR fee, regardless of the number of plan participants. The special rules that apply to Health Reimbursement Accounts (HRAs) and Health Flexible Spending Accounts (FSAs) are discussed below.

Plans exempt from the fee include:

If a plan sponsor maintains more than one self-insured plan, the plans can be treated as a single plan if they have the same plan year. For example, if an employer has a self-insured medical plan and a separate self-insured prescription drug plan with the same plan year, each employee, spouse and dependent covered under both plans is only counted once for purposes of the PCOR fee.

The IRS has created a helpful chart showing how the PCOR fee applies to common types of health plans.

Health Reimbursement Accounts (HRAs) - Nearly all HRAs are subject to the PCOR fee because they do not meet the conditions for exemption. An HRA will be exempt from the PCOR fee if it provides benefits only for dental or vision expenses, or it meets the following three conditions:

Health Flexible Spending Accounts (FSAs) - A health FSA is exempt from the PCOR fee if it satisfies an availability condition and a maximum benefit condition.

Additional special rules for HRAs and FSAs . Once an employer determines that its HRA or FSA is subject to the PCOR fee, the employer should consider the following special rules:

The IRS provides different rules for determining the average number of covered lives (i.e., employees, spouses and dependents) under insured plans versus self-insured plans. The same method must be used consistently for the duration of any policy or plan year. However, the insurer or sponsor is not required to use the same method from one year to the next.

A plan sponsor of a self-insured plan may use any of the following three

methods to determine the number of covered lives for a plan year:

1. Actual count method. Count the covered lives on each day of the plan year and divide by the number of days in the plan year.

Example: An employer has 900 covered lives on Jan. 1, 901 on Jan. 2, 890 on

Jan. 3, etc., and the sum of the lives covered under the plan on each day of

the plan year is 328,500. The average number of covered lives is 900 (328,500 ÷

365 days).

2. Snapshot method. Count the covered lives on a single day in each quarter (or more than one day) and divide the total by the number of dates on which a count was made. The date or dates must be consistent for each quarter. For example, if the last day of the first quarter is chosen, then the last day of the second, third and fourth quarters should be used as well.

Example: An employer has 900 covered lives on Jan. 15, 910 on April 15, 890 on

July 15, and 880 on Oct. 15. The average number of covered lives is 895 [(900 +

910+ 890+ 880) ÷ 4 days].

As an alternative to counting actual lives, an employer can count the number of

employees with self-only coverage on the designated dates, plus the number of

employees with other than self-only coverage multiplied by 2.35.

3. Form 5500 method. If a Form 5500 for a plan is filed before the due date of the Form 720 for that year, the plan sponsor can determine the number of covered lives based on the Form 5500. If the plan offers just self-only coverage, the plan sponsor adds the participant counts at the beginning and end of the year (lines 5 and 6d on Form 5500) and divides by 2. If the plan also offers family or dependent coverage, the plan sponsor adds the participant counts at the beginning and end of the year (lines 5 and 6d on Form 5500) without dividing by 2.

Example: An employer offers single and family coverage with a plan year ending

on Dec. 31. The 2013 Form 5500 is filed on June 5, 2014, and reports 132

participants on line 5 and 148 participants on line 6d. The number of covered

lives is 280 (132 + 148).

To evaluate liability for PCOR fees, plan sponsors should identify all of their plans that provide medical benefits and determine if each plan is insured or self-insured. If any plan is self-insured, the plan sponsor should take the following actions:

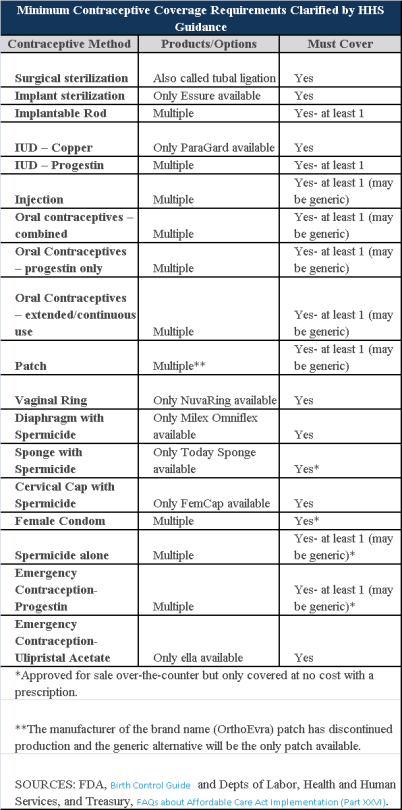

Plans and insurers must cover all 18 contraception methods approved by the U.S. Food and Drug Administration, according to a new set of questions and answers on the Affordable Care Act’s preventive care coverage requirements.

“Reasonable medical management” still may be used to steer members to specific products within those methods of contraception. A plan or insurer may impose cost-sharing on non-preferred items within a given method, as long as at least one form of contraception in each method is covered without cost-sharing.

However, an individual’s physician must be allowed to override the plan’s drug management techniques if the physician finds it medically necessary to cover without cost-sharing an item that a given plan or insurer has classified as non-preferred, according to one of the frequently asked questions from the U.S. Departments of Labor, Health and Human Services and the Treasury.

The ACA mandated all plans and insurers to cover preventive care items, as defined by the Public Health Service Act, without cost-sharing. Eighteen forms of female contraception are included under the preventive care list. The individual FAQs on contraception clarified the following requirements.

The FAQ comes just weeks after reports and news coverage detailed health plan violations of the women coverage provisions of the ACA.

Testing and Dependent Care Answers

In questions separate from contraception, plans and insurers were told they must cover breast cancer susceptibility (BRCA-1 or BRCA-2) testing without cost-sharing. The test identifies whether the woman has genetic mutations that make her more susceptible to BRCA-related breast cancer.

Another question stated that if colonoscopies are performed as preventive screening without cost-sharing, then plans could not impose cost-sharing on the anesthesia component of that service.

The U.S. Equal Employment Opportunity Commission (EEOC) recently issued proposed new rules clarifying its stance on the interplay between the Americans with Disabilities Act (ADA) and employer wellness programs. Officially called a “notice of proposed rulemaking” or NPRM, the new rules propose changes to the text of the EEOC’s ADA regulations and to the interpretive guidance explaining them.

If adopted, the NPRM will provide employers guidance on how they can use financial incentives or penalties to encourage employees to participate in wellness programs without violating the ADA, even if the programs include disability-related inquiries or medical examinations. This should be welcome news for employers, having spent nearly the past six years in limbo as a result of the EEOC’s virtual radio silence on this question.

A Brief History: How

Did We Get Here?

In 1990, the ADA was enacted to protect individuals with ADA-qualifying

disabilities from discrimination in the workplace. Under the ADA,

employers may conduct medical examinations and obtain medical histories as part

of their wellness programs so long as employee participation in them is

voluntary. The EEOC confirmed in 2000 that it considers a wellness

program voluntary, and therefore legal, where employees are neither required to

participate in it nor penalized for non-participation.

Then, in 2006, regulations were issued that exempted wellness programs from the nondiscrimination requirements of the Health Insurance Portability and Accountability Act (HIPAA) so long as they met certain requirements. These regulations also authorized employers for the first time to offer financial incentives of up to 20% of the cost of coverage to employees to encourage them to participate in wellness programs.

But between 2006 and 2009 the EEOC waffled on the legality of these financial incentives, stating that “the HIPAA rule is appropriate because the ADA lacks specific standards on financial incentives” in one instance, and that the EEOC was “continuing to examine what level, if any, of financial inducement to participate in a wellness program would be permissible under the ADA” in another.

Shortly thereafter, the 2010 enactment of President Obama’s Patient Protection and Affordable Care Act (ACA), which regulates corporate wellness programs, appeared to put this debate to rest. The ACA authorized employers to offer certain types of financial incentives to employees so long as the incentives did not exceed 30% of the cost of coverage to employees.

But in the years following the ACA’s enactment, the EEOC restated that it had not in fact taken any position on the legality of financial incentives. In the wake of this pronouncement, employers were left understandably confused and uncertain. To alleviate these sentiments, several federal agencies banded together and jointly issued regulations that authorized employers to reward employees for participating in wellness programs, including programs that involved medical examinations or questionnaires. These regulations also confirmed the previously set 30%–of-coverage ceiling and even provided for incentives of up to 50%of coverage for programs related to preventing or reducing the use of tobacco products.

After remaining silent about employer wellness programs for nearly five years, in August 2014, the EEOC awoke from its slumber and filed its very first lawsuit targeting wellness programs, EEOC v. Orion Energy Systems, alleging that they violate the ADA. In the following months, it filed similar suits against Flambeau, Inc., and Honeywell International, Inc. In EEOC v. Honeywell International, Inc., the EEOC took probably its most alarming position on the subject to date, asserting that a wellness program violates the ADA even if it fully complies with the ACA.

What’s In The NPRM?

According to EEOC Chair Jenny Yang, the purpose of the EEOC’s NPRM is to

reconcile HIPAA’s authorization of financial incentives to encourage

participation in wellness programs with the ADA’s requirement that medical

examinations and inquiries that are part of them be voluntary. To that

end, the NPRM explains:

Each of these parts of the NPRM is briefly discussed below.

What is an employee

wellness program?

In general, the term “wellness program” refers to a program or activity offered

by an employer to encourage its employees to improve their health and to reduce

overall health care costs. For instance, one program might encourage

employees to engage in healthier lifestyles, such as exercising daily, making

healthier diet choices, or quitting smoking. Another might obtain medical

information from them by asking them to complete health risk assessments or

undergo a screening for risk factors.

The NPRM defines wellness programs as programs that are reasonably designed to promote health or prevent disease. To meet this standard, programs must have a reasonable chance of improving the health of, or preventing disease in, its participating employees. The programs also must not be overly burdensome, a pretext for violating anti-discrimination laws, or highly suspect in the method chosen to promote health or prevent disease.

How is voluntary

defined?

The NPRM contains several requirements that must be met in order for

participation in wellness programs to be voluntary. Specifically,

employers may not:

Additionally, for wellness programs that are part of a group health plan, employers must provide a notice to employees clearly explaining what medical information will be obtained, how it will be used, who will receive it, restrictions on its disclosure, and the protections in place to prevent its improper disclosure.

What incentives may

you offer?

The NPRM clarifies that the offer of limited incentives is permitted and will

not render wellness programs involuntary. Under the NPRM, the maximum

allowable incentive employers can offer employees for participation in a

wellness program or for achieving certain health results is 30% of the total

cost of coverage to employees who participate in it. The total cost of

coverage is the amount that the employer and the employee pay, not just the

employee’s share of the cost. The maximum allowable penalty employers may

impose on employees who do not participate in the wellness program is the

same.

What about

confidentiality?

The NPRM does not change any of the exceptions to the confidentiality

provisions in the EEOC’s existing ADA regulations. It does, however, add

a new subsection that explains that employers may only receive information

collected by wellness programs in aggregate form that does not disclose, and is

not likely to disclose, the identity of the employees participating in it,

except as may be necessary to administer the plan.

Additionally, for a wellness program that is part of a group health plan, the health information that identifies an individual is “protected health information” and therefore subject to HIPAA. HIPAA mandates that employers maintain certain safeguards to protect the privacy of such personal health information and limits the uses and disclosure of it.

Keep in mind that the NPRM revisions discussed above only clarify the EEOC’s stance regarding how employers can use financial incentives to encourage their employees to participate in employer wellness programs without violating the ADA. It does not relieve employers of their obligation to ensure that their wellness programs comply with other anti-discrimination laws as well.

Is This The Law?

The NPRM is just a notice that alerts the public that the EEOC intends to

revise its ADA regulations and interpretive guidance as they relate to employer

wellness programs. It is also an open invitation for comments regarding

the proposed revisions. Anyone who would like to comment on the NPRM must

do so by June 19, 2015. After that, the EEOC will evaluate all of the

comments that it receives and may make revisions to the NPRM in response to

them. The EEOC then votes on a final rule, and once it is approved, it

will be published in the Federal Register.

Since the NPRM is just a proposed rule, you do not have to comply with it just yet. But our advice is that you bring your wellness program into compliance with the NPRM for a few reasons. For one, it is very unlikely that the EEOC, or a court, would fault you for complying with the NPRM until the final rule is published. Additionally, many of the requirements that are set forth in the NPRM are already required under currently existing law. Thus, while waiting for the EEOC to issue its final rule, in the very least, you should make sure that you do not:

In addition you should provide reasonable accommodations to employees with disabilities to enable them to participate in wellness programs and obtain any incentives offered (e.g., if an employer has a deaf employee and attending a diet and exercise class is part of its wellness program, then the employer should provide a sign language interpreter to enable the deaf employee to participate in the class); and ensure that any medical information is maintained in a confidential manner.

During this year, businesses will be hearing a lot about the Affordable Care Act’s (ACA’s) information reporting requirements under Code Sections 6055 and 6056. Information gathering will be critical to successful reporting, and there is one aspect of that information gathering which employers might want to take action on sooner rather than later – collecting Social Security numbers (SSNs), particularly when required to do so from the spouses and dependents of their employees. There are, of course, ACA implications for not taking this step, as well as data privacy and security risks for employer and their vendors.

Under the ACA, providers of “minimum essential coverage” (MEC) must report certain information about that coverage to the Internal Revenue Service (IRS), as well as to persons receiving that MEC. Employers that sponsor self-insured group health plans are providers of MEC for this purpose, and in the course of meeting the reporting requirements, must collect and report SSNs to the IRS. However, this reporting mandate requires those employers (or vendors acting on their behalf) to transmit to the IRS the SSNs of employee and their spouses and dependents covered under the plan, unless the employers either (i) exhaust reasonable collection efforts described below, (ii) or meet certain requirements for limited reporting overall.

Obviously, employers are familiar with collecting, using and disclosing employee SSNs for legitimate business and benefit plan purposes. Collecting SSNs from spouses and dependents will be an increased burden, creating more risk on employers given the increased amount of sensitive data they will be handling, and possibly from vendors working on their behalf. The reporting rules permit an employer to use a dependent’s date of birth, only if the employer was not able to obtain the SSN after “reasonable efforts.” For this purpose, reasonable efforts means the employer was not able to obtain the SSN after an initial attempt, and two subsequent attempts.

From an ACA standpoint, employers with self-insured plans that have not collected this information should be engaged in these efforts during the year (2015) to ensure they are ready either to report the SSNs, or the DOBs. At the same time, collecting more sensitive information about individuals raises data privacy and security risks for an organization regarding the likelihood and scope of a breach. Some of those risks, and steps employers could take to mitigate those risks, are described below.

Employers navigating through ACA compliance and reporting requirements have many issues to be considered. How personal information or protected health information is safeguarded in the course of those efforts is one more important consideration.

The IRS and the Treasury Department issued a notice on the so-called “Cadillac Tax”—a 40 percent excise tax to be imposed on high-cost employer-sponsored health plans beginning in 2018 under the Affordable Care Act (ACA).

Notice 2015-16, released on Feb. 23, 2015, discusses a number of issues concerning the tax and requests comments on the possible approaches that ultimately could be incorporated in proposed regulations. Specifically, the guidance states that the agencies anticipate that pretax salary reduction contributions made by employees to health savings accounts (HSAs) will be subject to the Cadillac tax.

Background

In 2018, the ACA provides that a nondeductible 40 percent excise tax be imposed on “applicable employer-sponsored coverage” in excess of statutory thresholds (in 2018, $10,200 for self-only, $27,500 for family). As 2018 approaches, the benefit community has long awaited guidance on this tax. While many employers have actively managed their plan offerings and costs in anticipation of the impact of the tax, those efforts have been hampered by the lack of guidance. Among other things, employers are uncertain what health coverage is subject to the tax and how the tax is calculated.

Particularly, Notice 2015-16 addresses:

The agencies are requesting comments on issues

discussed in this notice by May 15, 2015. They intend to issue another notice

that will address other areas of the excise tax and anticipates issuing

proposed regulations after considering public comments on both notices.

Applicable Coverage

Of most immediate interest to plan sponsors is the specific type of coverage (i.e., “applicable coverage”) that will be subject to the excise tax, particularly where the statute is unclear.

Employee Pretax HSA

Contributions

The ACA statute provides that employer contributions to an HSA are subject to

the excise tax, but did not specifically address the treatment of employee

pretax HSA contributions. The notice says that the agencies “anticipate that

future proposed regulations will provide that (1) employer contributions to

HSAs, including salary reduction contributions to HSAs, are included in

applicable coverage, and (2) employee after-tax contributions to HSAs are

excluded from applicable coverage.”

Note: This anticipated treatment of employee pretax contributions to HSAs will have a significant impact on HSA programs. If implemented as the agencies anticipate, it could mean many employer plans that provide for HSA contributions will be subject to the excise tax as early as 2018, unless the employer limits the amount an employee can contribute on a pretax basis.

Self-Insured Dental

and Vision Plans

The ACA statutory language specifically excludes fully insured dental and

vision plans from the excise tax. The treatment of self-insured dental and

vision plans was not clear. The notice states that the agencies will consider

exercising their “regulatory authority” to exclude self-insured plans that

qualify as excepted benefits from the excise tax.

Employee Assistance

Programs

The agencies are also considering whether to exclude excepted-benefit employee

assistance programs (EAPs) from the excise tax.

Onsite Medical Clinics

The notice discusses the exclusion of certain onsite medical clinics that offer

only de

minimis care to employees,

citing a provision in the COBRA regulations, and anticipates excluding such

clinics from applicable coverage. Under the COBRA regulations an onsite clinic

is not considered a group health plan if:

The agencies are also asking for comment on

the treatment of clinics that provide certain services in addition to first

aid:

In Closing

With the release of this initial guidance, plan sponsors can gain some insight into the direction the government is likely to take in proposed regulations and can better address potential plan design strategie

The Centers for Medicare & Medicaid Services (CMS) announced on February 20,2015 a special enrollment period (SEP) for individuals and families who did not have health coverage in 2014 and are subject to the fee or “shared responsibility payment” when they file their 2014 taxes in states which use the Federally-facilitated Marketplaces (FFM). This special enrollment period will allow those individuals and families who were unaware or didn’t understand the implications of this new requirement to enroll in 2015 health insurance coverage through the FFM.

For those who were unaware or didn’t understand the implications of the fee for not enrolling in coverage, CMS will provide consumers with an opportunity to purchase health insurance coverage from March 15 to April 30. If consumers do not purchase coverage for 2015 during this special enrollment period, they may have to pay a fee when they file their 2015 income taxes.

Those eligible for this special enrollment period live in states with a Federally-facilitated Marketplace and:

The special enrollment period announced today will begin on March 15, 2015 and end at 11:59 pm E.S.T. on April 30, 2015. If a consumer enrolls in coverage before the 15th of the month, coverage will be effective on the first day of the following month.

This year’s tax season is the first time individuals and families will be asked to provide basic information regarding their health coverage on their tax returns. Individuals who could not afford coverage or met other conditions may be eligible to receive an exemption for 2014. To help consumers who did not have insurance last year determine if they qualify for an exemption, CMS also launched a health coverage tax exemption tool today on HealthCare.gov and CuidadodeSalud.gov.

“We recognize that this is the first tax filing season where consumers may have to pay a fee or claim an exemption for not having health insurance coverage,” said CMS Administrator Marilyn Tavenner. “Our priority is to make sure consumers understand the new requirement to enroll in health coverage and to provide those who were not aware or did not understand the requirement with an opportunity to enroll in affordable coverage this year.”

Most taxpayers will only need to check a box when they file their taxes to indicate that they had health coverage in 2014 through their employer, Medicare, Medicaid, veterans care or other qualified health coverage that qualifies as “minimum essential coverage.” The remaining taxpayers will take different steps. It is expected that 10 to 20 percent of taxpayers who were uninsured for all or part of 2014 will qualify for an exemption from the requirement to have coverage. A much smaller fraction of taxpayers, an estimated 2 to 4 percent, will pay a fee because they made a choice to not obtain coverage and are not eligible for an exemption.

Americans who do not qualify for an exemption and went without health coverage in 2014 will have to pay a fee – $95 per adult or 1 percent of their income, whichever is greater – when they file their taxes this year. The fee increases to $325 per adult or 2% of income for 2015. Individuals taking advantage of this special enrollment period will still owe a fee for the months they were uninsured and did not receive an exemption in 2014 and 2015. This special enrollment period is designed to allow such individuals the opportunity to get covered for the remainder of the year and avoid additional fees for 2015.

The Administration is committed to providing the information and tools tax filers need to understand the new requirements. Part of this outreach effort involves coordinating efforts with nonprofit organizations and tax preparers who provide resources to consumers and offer on the ground support. If consumers have questions about their taxes, need to download forms, or want to learn more about the fee for not having insurance, they can find information and resources at www.HealthCare.gov/Taxes or www.IRS.gov. Consumers can also call the Marketplace Call Center at 1-800-318-2596. Consumers who need assistance filing their taxes can visit IRS.gov/VITA or IRS.gov/freefile.

Consumers seeking to take advantage of the special enrollment period can find out if they are eligible by visitinghttps://www.healthcare.gov/get-coverage. Consumers can find local help at: Localhelp.healthcare.gov or call the Federally-facilitated Marketplace Call Center at 1-800-318-2596. TTY users should call 1-855-889-4325. Assistance is available in 150 languages. The call is free.

For more information about Health Insurance Marketplaces, visit: www.healthcare.gov/marketplace

Last week, the IRS issued its “final” versions of the forms 1094-B,1094-C, 1095-B and 1095-C along with instructions for the “B” forms and instructions for the “C” forms. The good news is that the forms are pretty much the same from the drafts released in mid 2014. What has changed is that the revised instructions have filled in some gaps about reporting, some of which are highlighted below:

1. Employers with 50-99 FTEs who were exempt from compliance in 2015 must still file these forms for the 2015 tax year.

2. For employers that cover non-employees (COBRA beneficiaries or retirees being most common), they can use forms 1094-B and 1095-B instead of filing out 1095-C Part III to report for those individuals.

3. With respect to reporting for employees who work for more than one employer member of a controlled group aggregated “ALE”, the employee may receive a report from each separate employer. However, the employer for whom he or she works the most hours in a given month should report for that month.

4. Under the final instructions, a full-time employee of a self-insured employer that accepts a qualifying offer and enrolls in coverage, the employer must provide that employee a 1095-C. The previous draft indicated that it would be enough to simply provide an employee a statement about the offer rather than an actual form

5. For plans that exclude spouses covered or offered health coverage through their own employers, the definition of “offer of health coverage” now provides that an offer to a spouse subject to a reasonable, objective condition is treated as an offer of coverage for reporting purposes.

6. There are some changes with respect to what days can be used to measure the “count” for reporting purposes. Employers are allowed to use the first day of the first payroll period of each month or the last day of the first payroll period of each month, as long as the last day is in the same month as when the payroll period starts. Also, an employer can report offering coverage for a month only if the employer offers coverage for every day of that month. Mid-month eligibilities would presumably be counted as being covered on the first day of the next month. However, in the case of terminations of employment mid-month, the coverage can be treated as offered for the entire month if, but for the termination, the coverage would have continued for the full month.

Now as a refresher about what needs to be filed:

Bear in mind that there is a considerable amount of time between now and the final filing obligation so there may be additional revisions to these instructions, or at least some further clarification. But in the meantime, read the instructions and familiarize yourself with the reporting obligations as well as beginning the steps to collecting the necessary data to make completing the forms next year easier.

The Affordable Care Act will require Applicable Large Employers (i.e. large employers subject to the employer mandate) and employers sponsoring self-insured plans to comply with new annual IRS reporting requirements. The first reporting deadline will be February 28, 2016 as to the data employers collect during the 2015 calendar year. The reporting provides the IRS with information it needs to enforce the Individual Mandate (i.e. individuals are penalized for not having health coverage) and the Employer Mandate (i.e. large employers are penalized for not offering health coverage to full-time employees). The IRS will also require employers who offer self-insured plans to report on covered individuals.

Large employers and coverage providers must also provide a written statement to each employee or responsible individual (i.e. one who enrolls one or more individuals) identifying the reported information. The written statement can be a copy of the Form.

The IRS recently released draft Forms 1094-C and 1095-C and draft Forms 1094-B and 1095-B, along with draft instructions for each form.

Which Forms Do I File?

When?

Statements to employees and responsible individuals are due annually by January 31. The first statements are due January 31, 2016.

Forms 1094-B, 1095-B, 1094-C and 1095-C are due annually by February 28 (or by March 31, if filing electronically). The first filing is due by February 28, 2016 (or March 31, 2016, if filing electronically).

Even though the forms are not due until 2016, the annual reporting will be based on data from the prior year. Employers need to plan ahead now to collect data for 2015. Many employers have adopted the Look Back Measurement Method Safe Harbor (“Safe Harbor”) to identify full-time employees under the ACA. The Safe Harbor allows employers to “look back” on the hours of service of its employees during 2014 or another measurement period. There are specific legal restrictions regarding the timing and length of the periods under the Safe Harbor, so employers cannot just pick random dates. Employers also must follow various rules to calculate hours of service under the Safe Harbor. The hours of service during the measurement period (which is likely to include most of 2014) will determine whether a particular employee is full-time under the ACA during the 2015 stability period. The stability period is the time during which the status of the employee, as full-time or non-full-time, is locked in. In 2016, employers must report their employees’ full-time status during the calendar year of 2015. Therefore, even though the IRS forms are not due until 2016, an employee’s hours of service in 2014 will determine how an employer reports that employee during each month of 2015. Employers who have not adopted the Safe Harbor should consider doing so because it allows an employer to average hours of service over a 12-month period to determine the full-time status of an employee. If an employer does not adopt the Safe Harbor, the IRS will require the employer to make a monthly determination, which is likely to increase an employer’s potential exposure to penalties.

What Must the Employer Report?

Form 1095-C

There are three parts to Form 1095-C. An applicable large employer must file one Form 1095-C for each full-time employee. If the applicable large employer sponsors self-insured health plans, it must also file Form 1095-C for any employee who enrolls in coverage regardless of the full-time status of that employee.

Form 1095-C requires the employer to identify the type of health coverage offered to a full-time employee for each calendar month, including whether that coverage offered minimum value and was affordable for that employee. Employers must use a code to identify the type of health coverage offered and applicable transition relief.

Employers that offer self-insured health plans also must report information about each individual enrolled in the self-insured health plan, including any full-time employee, non-full-time employee, employee family members, and others.

Form 1094-C

Applicable large employers use Form 1094-C as a transmittal to report employer summary information and transmit its Forms 1095-C to the IRS. Form 1094-C requires employers to enter the name and contact information of the employer and the total number of Forms 1095-C it submits. It also requires information about whether the employer offered minimum essential coverage under an eligible employer-sponsored plan to at least 95% of its full-time employees and their dependents for the entire calendar year, the number of full-time employees for each month, and the total number of employees (full-time or non-full-time) for each month.

Form 1095-B

Employers offering self-insured coverage use Form 1095-B to report information to the IRS about individuals who are covered by minimum essential coverage and therefore are not liable for the individual shared responsibility payment. These employers must file a Form 1095-B for eachindividual who was covered for any part of the calendar year. The employer must make reasonable efforts to collect social security numbers for covered individuals.

Form 1094-B

Employers who file Form 1095-B will use Form 1094-B as a transmittal form. It asks for the name of the employer, the employer’s EIN, and the name, telephone number, and address of the employer’s contact person.

Failure to Report – What Happens?

The IRS will impose penalties for failure to timely provide correct written statements to employees. The IRS will also impose penalties for failure to timely file a correct return. For the 2016 reporting on 2015 data, the IRS will not impose a penalty for good faith compliance. However, the IRS specified that good faith compliance requires that employers provide the statements and file the returns.

On November 4, 2014, the IRS released Notice 2014-69 which outlines that health plans that fail to provide substantial coverage for in-patient hospitalization services or for physician services (or both) referred to as Non-Hospital/Non-Physician Services Plan) are now not considered as providing the minimum value coverage as intended by the minimum value plan requirements for the employer mandate under ACA.

For employers who have already entered into a binding written commitment to adopt, or have begun enrolling employees in, a Non-Hospital/Non-Physician Services Plan prior to November 4, 2014, they will not be penalized for not meeting the employer mandate for the 2015 plan year if that plan year begins no later than March 1, 2015. This is based on the employer’s reliance on the results of the Minimum Value Calculator (a Pre-November 4, 2014 Non-Hospital/Non-Physician Services Plan) as outlined in previous guidance.

For employers who have not entered in to a written commitment to adopt, have not begun enrolling employees in a Non-Hospital/Non-Physician Services Plan on or after November 4, 2014, or have a plan year that begins after March 1,2015, no relief will be given under the employer mandate.

Pending final regulations, employees will not be required to treat a Non-Hospital/Non-Physician Services Plan as providing minimum value coverage for purposes of determining their eligibility for a premium tax credit “aka premium subsidy” in the Marketplace.

An employer that offers a Non-Hospital/Non-Physician Services Plan (including a Pre-November 4, 2014 Non-Hospital/Non-Physician Services Plan) to an employee:

(1) must not state or imply in any disclosure that the offer of coverage under the Non-Hospital/Non-Physician Services Plan prevents an employee from obtaining a premium tax credit, if otherwise eligible, and

(2) must timely correct any prior disclosures that stated or implied that the offer of the Non-Hospital/Non-Physician Services Plan would prevent an otherwise tax-credit-eligible employee from obtaining a premium tax credit.

Without such a corrective disclosure, a statement a Non-Hospital/Non-Physician Services Plan provides minimum value will be considered to imply that the offer of such a plan prevents employees from obtaining a premium tax credit/subsidy. However, an employer that also offers an employee another plan that is not a Non-Hospital/Non/-Physician Services Plan and that is affordable and provides minimum value is permitted to advise the employee that the offer of this other plan will or may preclude the employee from obtaining a premium tax credit.

The deadline for submitting the required information and scheduling the requirement payment, which must be done through www.pay.gov is November 15, 2014.

The Affordable Care Act (ACA) provides for a transitional reinsurance program to help stabilize premiums for coverage in the individual health insurance marketplace during the first 3 years of operation (2014-2016). The program is designed to primarily transfer funds from the group market to the individual market, where high risk individuals are more likely to be covered.

Payments under the reinsurance program are funded by “contributions” (aka fees) payable by health insurance carriers for fully funded groups and third party administrators on behalf of self-insured group health plans. However, under ACA regulations, the self insured group is ultimately responsible for the payment.

The transitional reinsurance fee requirement applies on a per capita basis with respect to each individual covered by a plan that is subject to the fee. The total amount of the fee for 2014 is $63 per covered life and will decrease to $44 per covered life in 2015. The amount of the fee in 2016 has not yet been established by CMS, but will be lower than the 2015 amount. The fee applies to major medical coverage, retiree medical coverage, and COBRA coverage. Plans that are not subject to the reinsurance fee include FSAs, HSAs, Dental & Vision coverage, coverage that fails to provide minimum value, and EAP programs to name a few.

The transitional reinsurance fee is imposed on the “contributing entity”, defined as an insurer/carrier for fully-insured coverage or the group for self insured coverage. Third -party administrators (TPAs), administrative service only entities (ASO) and others may submit on behalf of the contributing entity, though CMS has specified that the TPA or ASO is not required by law to do so.

Because the fee is imposed on the self insured plan and not the plan sponsor, plan assets may be used to pay the assessment/fee. The IRS has also noted that plan sponsors can treat the fee as an ordinary and necessary business expense for tax purposes.

The term covered lives includes everyone under the plan, including spouses, dependents, and retirees. CMS has named several options for counting covered lives, depending on if the plan is fully insured or self funded. The methods of counting covered lives for the reinsurance fee are similar to, but not exactly the same, as the Patient Centered Outcomes Research Institute (PCORI) count methods. A full description of each counting method can be found on the CMS website here.

Regardless of the counting method chosen, plans must maintain documentation of the count, including all materials provided by TPAs in arriving at the figure, for at least 10 years. CMS may audit a plan to assess its compliance with the program requirements and it will be crucial to be able to produce this information.

The entire reinsurance fee process takes place on www.pay.gov. This process is separate from the Health Insurance Oversight System (HIOS) which is used, for example, to obtain a Health Plan Identifier (HPID). The applicable form became available on October 24, 2014. While this leaves somewhat limited time for plan sponsors to submit the applicable form and schedule the fee by the November 15, 2014 deadline, CMS has yet to issue guidance that the submission date will be delayed.

In order to successfully complete the reinsurance fee submission, plan sponsors (or their representatives) need to:

After registering on Pay.gov, the submitter will select the Transitional Reinsurance program Annual Enrollment and Contribution Submission Form. The form requires basic company and contact info, payment type, benefit year, and the annual enrollment count. After the information is entered on the form, plan sponsors will need to upload their supporting documentation CSV file. After the enrollment and supporting documentation is submitted, the form will auto-calculate the amount owed. Plans then need to schedule payment(s) for this amount . The form cannot be submitted without payment information. Plans can choose to remit payment for the entire benefit year once (the full $63 per covered life) or plans can submit two separate payments for the year. If the separate payment method is used, the first payment ($52.50 per covered life) is due by January 15, 2015 and the second payment ($10.50 per covered life) is due by November 15, 2015. Regardless of the option chose, all payments MUST be scheduled by November 15, 2014.