Page 2 of 2

Earlier this week, President Obama signed the 21st Century Cures Act (“Act”). This Act contains provisions for “Qualified Small Business Health Reimbursement Arrangements” (“HRA”). This new HRA would allow eligible small employers to offer a health reimbursement arrangement funded solely by the employer that would reimburse employees for qualified medical expenses including health insurance premiums.

The maximum reimbursement that can be provided under the plan is $4,950 or $10,000 if the HRA provided for family members of the employee. An employer is eligible to establish a small employer health reimbursement arrangement if that employer (i) is not subject to the employer mandate under the Affordable Care Act (i.e., less than 50 full-time employees) and (ii) does not offer a group health plan to any employees.

To be a qualified small employer HRA, the arrangement must be provided on the same terms to all eligible employees, although the Act allows benefits under the HRA to vary based on age and family-size variations in the price of an insurance policy in the relevant individual health insurance market.

Employers must report contributions to a reimbursement arrangement on their employees’ W-2 each year and notify each participant of the amount of benefit provided under the HRA each year at least 90 days before the beginning of each year.

This new provision also provides that employees that are covered by this HRA will not be eligible for subsidies for health insurance purchased under an exchange during the months that they are covered by the employer’s HRA.

Such HRAs are not considered “group health plans” for most purposes under the Code, ERISA and the Public Health Service Act and are not subject to COBRA.

This new provision also overturns guidance issued by the Internal Revenue Service and the Department of Labor that stated that these arrangements violated the Affordable Care Act insurance market reforms and were subject to a penalty for providing such arrangements.

The previous IRS and DOL guidance would still prohibit these arrangements for larger employers. The provision is effective for plan years beginning after December 31, 2016. (There was transition relief for plans offering these benefits that ends December 31, 2016 and extends the relief given in IRS Notice 2015-17.)

In a first-of-its-kind decision, a federal court recently upheld the right of employees to sue their employer for allegedly cutting employee hours to less than 30 hours per week to avoid offering health insurance under the Affordable Care Act (ACA). Specifically, the District Court for the Southern District of New York denied a defense Motion to Dismiss in a case where a group of workers allege that Dave & Buster’s (a national restaurant and entertainment chain) “right-sized” its workforce for the purpose of avoiding healthcare costs.

Although this case is in the very early stages of litigation and is far from being decided, you should monitor this for developments to determine whether you need to take action to deter potential copycat lawsuits.

One of the initial concerns by ACA critics is that many employers would respond to the Employer Mandate by reducing full-time employee hours to avoid the coverage obligation and associated penalties, increasing the number of part-time workers in the national economy. This is because the ACA does not require an employer to offer affordable, minimum-value coverage to employees generally working less than 30 hours per week.

Although the initial economic data analyzing the national workforce suggests that the predictions of wide-scale reduction in employee hours have not materialized, some employers have increased their reliance on part-time employees as an ACA strategy to manage the costs of the Employer Mandate.

Section 510 of ERISA prohibits discrimination and retaliation against plan participants and beneficiaries with respect to their rights to benefits. More specifically, ERISA Section 510 prohibits employers from interfering “with the attainment of any right to which such participant may become entitled under the plan.” Because many employment decisions affect the right to present or future benefits, courts generally require that plaintiffs show specific employer intent to interfere with benefits if they want to successfully assert a cause of action under ERISA Section 510.

The court found that the class of plaintiffs showed sufficient evidence in support of their claim that their participation in the health insurance plan was discontinued because the employer acted with “unlawful purpose” in realigning its workforce to avoid ACA-related costs. In this regard, the employees claimed that the company held meetings during which managers explained that the ACA would cost millions of dollars, and that employee hours were being reduced to avoid that cost.

However, if you are considering reducing your employee hours, you should carefully consider how such reductions are communicated to your workforce. Employers often have varied reasons for reducing employee hours, and many of those reasons have legitimate business purposes. It is vital that any communications made to your employees about such reductions describe the underlying rationale with clarity.

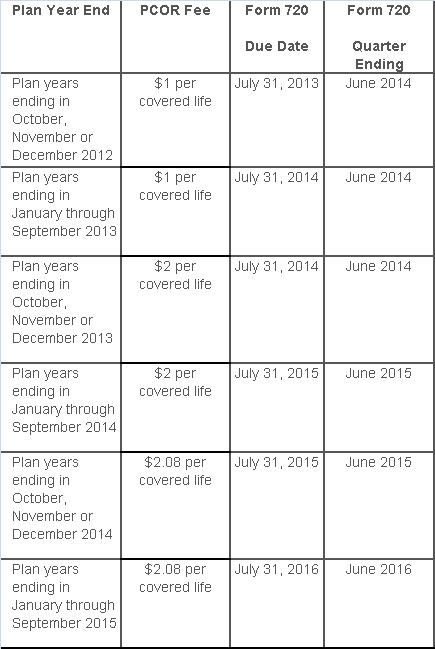

The Affordable Care Act added a patient-centered outcomes research (PCOR) fee on health plans to support clinical effectiveness research. The PCOR fee applies to plan years ending on or after Oct. 1, 2012, and before Oct. 1, 2019. The PCOR fee is due by July 31 of the calendar year following the close of the plan year. For plan years ending in 2014, the fee is due by July 31, 2015.

PCOR fees are required to be reported annually on Form 720, Quarterly Federal Excise Tax Return, for the second quarter of the calendar year. The due date of the return is July 31. Plan sponsors and insurers subject to PCOR fees but not other types of excise taxes should file Form 720 only for the second quarter, and no filings are needed for the other quarters. The PCOR fee can be paid electronically or mailed to the IRS with the Form 720 using a Form 720-V payment voucher for the second quarter. According to the IRS, the fee is tax-deductible as a business expense.

The PCOR fee is assessed based on the number of employees, spouses and dependents that are covered by the plan. The fee is $1 per covered life for plan years ending before Oct. 1, 2013, and $2 per covered life thereafter, subject to adjustment by the government. For plan years ending between Oct. 1, 2014, and Sept. 30, 2015, the fee is $2.08. The Form 720 instructions are expected to be updated soon to reflect this increased fee.

This chart summarizes the fee schedule based on the plan year end and shows the Form 720 due date. It also contains the quarter ending date that should be reported on the first page of the Form 720 (month and year only per IRS instructions). The plan year end date is not reported on the Form 720.

For insured plans, the insurance company is responsible for filing Form 720 and paying the PCOR fee. Therefore, employers with only fully- insured health plans have no filing requirement.

If an employer sponsors a self-insured health plan, the employer must file Form 720 and pay the PCOR fee. For self-insured plans with multiple employers, the named plan sponsor is generally required to file Form 720. A self-insured health plan is any plan providing accident or health coverage if any portion of such coverage is provided other than through an insurance policy.

Since the fee is a tax assessed against the plan sponsor and not the plan, most funded plans subject to ERISA must not pay the fee using plan assets since doing so would be considered a prohibited transaction by the U.S. Department of Labor (DOL). The DOL has provided some limited exceptions to this rule for plans with multiple employers if the plan sponsor exists solely for the purpose of sponsoring and administering the plan and has no source of funding independent of plan assets.

Plans sponsored by all types of employers, including tax-exempt organizations and governmental entities, are subject to the PCOR fee. Most health plans, including major medical plans, prescription drug plans and retiree-only plans, are subject to the PCOR fee, regardless of the number of plan participants. The special rules that apply to Health Reimbursement Accounts (HRAs) and Health Flexible Spending Accounts (FSAs) are discussed below.

Plans exempt from the fee include:

If a plan sponsor maintains more than one self-insured plan, the plans can be treated as a single plan if they have the same plan year. For example, if an employer has a self-insured medical plan and a separate self-insured prescription drug plan with the same plan year, each employee, spouse and dependent covered under both plans is only counted once for purposes of the PCOR fee.

The IRS has created a helpful chart showing how the PCOR fee applies to common types of health plans.

Health Reimbursement Accounts (HRAs) - Nearly all HRAs are subject to the PCOR fee because they do not meet the conditions for exemption. An HRA will be exempt from the PCOR fee if it provides benefits only for dental or vision expenses, or it meets the following three conditions:

Health Flexible Spending Accounts (FSAs) - A health FSA is exempt from the PCOR fee if it satisfies an availability condition and a maximum benefit condition.

Additional special rules for HRAs and FSAs . Once an employer determines that its HRA or FSA is subject to the PCOR fee, the employer should consider the following special rules:

The IRS provides different rules for determining the average number of covered lives (i.e., employees, spouses and dependents) under insured plans versus self-insured plans. The same method must be used consistently for the duration of any policy or plan year. However, the insurer or sponsor is not required to use the same method from one year to the next.

A plan sponsor of a self-insured plan may use any of the following three

methods to determine the number of covered lives for a plan year:

1. Actual count method. Count the covered lives on each day of the plan year and divide by the number of days in the plan year.

Example: An employer has 900 covered lives on Jan. 1, 901 on Jan. 2, 890 on

Jan. 3, etc., and the sum of the lives covered under the plan on each day of

the plan year is 328,500. The average number of covered lives is 900 (328,500 ÷

365 days).

2. Snapshot method. Count the covered lives on a single day in each quarter (or more than one day) and divide the total by the number of dates on which a count was made. The date or dates must be consistent for each quarter. For example, if the last day of the first quarter is chosen, then the last day of the second, third and fourth quarters should be used as well.

Example: An employer has 900 covered lives on Jan. 15, 910 on April 15, 890 on

July 15, and 880 on Oct. 15. The average number of covered lives is 895 [(900 +

910+ 890+ 880) ÷ 4 days].

As an alternative to counting actual lives, an employer can count the number of

employees with self-only coverage on the designated dates, plus the number of

employees with other than self-only coverage multiplied by 2.35.

3. Form 5500 method. If a Form 5500 for a plan is filed before the due date of the Form 720 for that year, the plan sponsor can determine the number of covered lives based on the Form 5500. If the plan offers just self-only coverage, the plan sponsor adds the participant counts at the beginning and end of the year (lines 5 and 6d on Form 5500) and divides by 2. If the plan also offers family or dependent coverage, the plan sponsor adds the participant counts at the beginning and end of the year (lines 5 and 6d on Form 5500) without dividing by 2.

Example: An employer offers single and family coverage with a plan year ending

on Dec. 31. The 2013 Form 5500 is filed on June 5, 2014, and reports 132

participants on line 5 and 148 participants on line 6d. The number of covered

lives is 280 (132 + 148).

To evaluate liability for PCOR fees, plan sponsors should identify all of their plans that provide medical benefits and determine if each plan is insured or self-insured. If any plan is self-insured, the plan sponsor should take the following actions:

Healthcare Reform continues to roll on despite all of its opponents. While 2014 brought the implementation of the health insurance exchanges, the Individual Mandate, and a host of new rules relating to employer-provided health coverage, 2015 marks the start of yet another major component of the Affordable Care Act (ACA): the Employer Mandate.

In the a recent article written by Fisher & Phillips LLP attorney Steven Witt, he discusses the potential risks employers can face if they are not careful in how they implement (and document) their compliance strategies with regards to the Employer Mandate.

The Employer Mandate requires large employers to offer compliant group health coverage to their “full-time employees” and their dependents or face excise tax penalties. Say you are a large employer who has never offered health insurance (or perhaps only to a small subset of your employees). You do not want to bankrupt the company and offer health insurance to your entire workforce, nor do you want to face tax penalties. Instead, you opt for what the Employer Mandate calls for: you offer health insurance coverage to only your full-time employees.

If you decide to only offer coverage to your “full-time” employees, simply setting measurement period dates with your human resources department and running payroll reports to determine who is “full-time” will not sufficiently limit the risk of controversy and potential legal liability. You will be much better off to clearly define these eligibility rules in writing and make sure any old, conflicting eligibility rules are updated.

Leaving existing plan documents and other materials (e.g., employee handbooks) to define health insurance eligibility with something vague like “full-time employees: employees who regularly work 30 or more hours per week,” is only inviting trouble. You will no doubt have employees (with attorneys) who could make plausible arguments that they “regularly” work 30 or more hours a week and can point to your existing written documents as evidence they should have been offered health insurance. Without clearly setting out new eligibility rules, it will be a much steeper uphill battle for the employer to defend itself.

On the other hand, if such employees attempt to claim that they were unfairly denied health insurance coverage, an employer should be on much stronger footing to defend its position that those employees are not “full-time” if it can point to written documentation outlining items such as (a) date ranges used for measurement periods and stability periods; (b) waiting periods for newly-eligible employees; and © how to treat employees in special circumstances, such as those who are promoted from a part-time position to a full-time position, those on a leave of absence, or rehired employees.

If you have not already done this, it is not too late. Even employers subject to the Employer Mandate in 2015 can still timely revise their SPDs or perhaps draft stand-alone benefits eligibility documents or other “wrap” documents to fully outline new eligibility rules. Steven advises employers to pay close attention as additional regulations and agency guidance continues to roll out to ensure they stay in compliance with ERISA, the ACA, and other related federal and state health insurance-related laws.

In short, it depends.

Recently, several clients have received their annual premium rebate checks from their group health insurance company and are looking for guidance on the proper use of these funds. Under the Patient Protection and Affordable Care Act (“PPACA”), it requires health insurance companies now operate on specific medical loss ratios (80% for employers with less than 100 employees and 85% for employers with more than 100 lives). If an insurance company does not meet the stated medical loss ratios (MLRs), it is required to rebate part of the premium received back to groups.

Below is a summarized analysis used to determine if an employer can keep the premium rebate in whole or in part:

Plan Assets: The first step is to determine who owns the rebate. In accordance with the DOL’s guidance (Technical Release 2011-04), the portion of the rebate that is attributable to employee contributions is considered a plan asset. Therefore, if employees contributed to the cost of the group medical insurance plan, they are entitled a percentage of the rebate equal to the cost paid by the employees (i.e.- if employees paid 25% of the premiums, they would be entitled to 25% of the rebate). If the employer paid the entire cost of the premium, then no part of the rebate would be attributable to employee contributions permitting the employer to retain the full rebate.

For further guidance on premium rebates or any of the PPACA or ACA requirements for employers, please contact our office.

The topic this month highlights record retention and cover what employers should be keeping and for how long.

Did you know that there are over 14,000 federal, state, and industry specific laws/standards/regulations that dictate how long employers are required to keep certain records? Non-compliance can result in fines against company employees personally as well as judgments against the company itself.

Some of the Federal Labor and Employment laws that require record retention include:

Please contact our office directly if you would like more information on this topic or if you would like more information regarding how to conduct an audit of your company record retention policies.