As the economy remains resilient, companies are in a battle not only to hire capable talent, but also to retain the workers that are assets to the organization. Much has been written about the impact of the Baby Boomers and Millennials in the workplace. However, what about the smaller Generation X cohort that is sometimes the forgotten middle child of the generations? While they may be outnumbered by the Millennials and Boomers, their influence has shaped US companies during years of technological advancement and corporate change. What are the characteristics of Gen X, and what do they want from their employer?

Independent

The Gen X group born between 1965-1980 was often referred to as latchkey kids. This term was used because a number of them came home alone after school because both parents worked. This fostered a sense of self discipline and autonomy. These individuals had to self-manage their own activities and make decisions based on judgment in the absence of an adult. Gen X learned not to depend on others for constant direction; they created their own outcomes.

Adaptable

Gen Xers childhood predated the internet, personal home computers, and cell phones. They had to learn evolving technology as well as embrace and master it to be successful in corporate America. From the generation that used the first cordless home phone, to commanding the world of work on a smartphone, their actions illustrate the ability to adapt, pivot, and embrace change.

Self-Reliant

This cohort has experienced two Gulf Wars, dot com bust, 9/11 tragedy, The Great Recession, and COVID. All of these events came with a great loss of jobs and retraction of the economy. Gen Xers have managed to navigate some of the most unprecedented events in history that impacted careers and livelihoods. Their resourcefulness helped them thrive and develop the expertise needed to stay relevant in the workforce in the midst of those events.

Growth and Development

Invest in Gen X workers continued growth and development. Whether it be formal classroom leadership training, conferences and seminars, or online courses, help them enhance their skill set. They already have a wealth of business acumen, so modernizing their tool kit benefits them and improves results for the organization. Most of Gen X has been working for decades, and any job can become repetitive and monotonous if skill sets become stagnant. Create a culture of learning and design training programs that address the needs of mid-career professionals.

New Projects & Meaningful Work

Invite them to lead new company projects and initiatives. In addition, consider offering Gen Xers a different role outside of their comfort zone that teaches them a new talent. They likely have a distinguished track record of tackling new assignments, so keep them energized with new leadership responsibilities. Evaluate your process for promotions. Is it based on performance data? Many in this group want to achieve the next level of success within a company. Engage in dialogue and determine what is important to them in their career trajectory.

Flexibility

Some Gen Xers want enhanced flexibility to care for children, parents, or pursue outside interests. Flexibility desires may reach beyond the ability to work from home periodically. Moreover, some may want to take on a part time role or become an independent contractor supporting their current team. Some workers may simply want more vacation days. One size does not fit all when it comes to flexibility, and people have different motivators – ask them.

Mentor Others

Every organization is engaged in succession planning as the life line for business continuity. Gen X is an irreplaceable asset of industry knowledge and expertise. Many want to mentor, teach, and help the next generation succeed in their careers. They have a command of workplace dynamics and want to impart their skills and coach new leaders to excel in the organization.

The Generation X Influence

As pivotal members of corporate work teams, Gen X is 53 million strong in the US labor force. This group is often described as autonomous but driven to make a difference and have an impact. By using different methods to engage Gen X, we can align to their values and retain them for decades.

There are two potential ACA employer mandate penalties that can impact ALEs:

a) IRC §4980H(a)—The “A Penalty”

The first is the §4980H(a) penalty—frequently referred to as the “A Penalty” or the “Sledge Hammer Penalty.” This penalty applies where the ALE fails to offer minimum essential coverage to at least 95% of its full-time employees in any given calendar month.

The 2022 A Penalty is $229.17/month ($2,750 annualized) multiplied by all full-time employees (reduced by the first 30). It is triggered by at least one full-time employee who was not offered minimum essential coverage enrolling in subsidized coverage on the Exchange. Note: The IRS has not yet released the 2023 A Penalty increase.

The “A Penalty” liability is focused on whether the employer offered a major medical plan to a sufficient percentage of full-time employees—not whether that offer was affordable (or provided minimum value).

b) IRC §4980H(b)—The “B Penalty”

The second is the §4980H(b) penalty—frequently referred to as the “B Penalty or the “Tack Hammer Penalty.” This penalty applies where the ALE is not subject to the A Penalty (i.e., the ALE offers coverage to at least 95% of full-time employees).

The B Penalty applies for each full-time employee who was:

Only those full-time employees who enroll in subsidized coverage on the Exchange will trigger the B Penalty. Unlike the A Penalty, the B Penalty is not multiplied by all full-time employees.

In other words, an ALE who offers minimum essential coverage to a full-time employee will be subject to the B Penalty if:

The 2022 B Penalty is $343.33/month ($4,120 annualized) per full-time employee receiving subsidized coverage on the Exchange. Note: The IRS has not yet released the 2023 B Penalty increase.

If you accepted expired forms of identification from new employees who completed their I-9 forms during the pandemic, your deadline for updating them with current proofs of identification is fast approaching. The Department of Homeland Security recently announced that it was winding down its temporary policy that had allowed for expired List B (proof of identification) documents to be used when completing I-9s because of COVID-related difficulties in renewing such I.D. documents. You have until July 31 to update your I-9 forms to get into compliance with the law. What do you need to know about this fast-approaching deadline?

How We Ended Up Where We Are

In response to the COVID-19 pandemic, the Department of Homeland Security issued a number of temporary policies easing Form I-9 compliance. One of them was the COVID-19 Temporary Policy for List B Identity Documents.

Under this policy, employers were allowed to accept expired List B (proof of identification) documents. Many state and local agencies were under lockdown, so it was difficult – if not impossible – for individuals to renew expired documents such as drivers’ licenses, school I.D. cards, Native American tribal documents, and others.

What’s Changed?

The Department rescinded this temporary policy on May 1 and began again to require employers to accept only unexpired List B documents. USICS recently announced that employers who accepted expired List B documents prior to May 1, 2022, will have until July 31,2022 to update their Forms I-9.

What Should You Do?

Specifically, for employees hired between May 1, 2020 and April 30, 2022 who presented an expired List B document, you need to have them to present to you:

Important Notes

You do not need to update documents for affected employees who are no longer employed.

When updating List B documentation, you should enter the document’s:

Your representative should initial and date the change.

If the List B document was auto-extended by the issuing authority, making it unexpired when it was presented, no update is needed. For example, many states automatically extended the expiration date of certain drivers’ licenses due to COVID. Those documents would not need updating.

Remote I-9 Verification Remains in Place – For Now

This move by DHS does not affect its decision to extend its remote I-9 verification flexibility policy, which has been extended once again to October 31, 2022.

Under that temporary policy, if employees hired on or after April 1, 2021, work exclusively in a remote setting due to COVID-19-related precautions, they are temporarily exempt from the I-9’s physical inspection requirements until they undertake non-remote employment on a regular, consistent, or predictable basis, or the extension of the flexibilities related to such requirements is terminated by DHS, whichever is earlier.

Conclusion

With these constantly evolving rules, employers who have adjusted their document inspection protocols during the pandemic may be at a higher risk for expensive monetary fines, potentially running in the thousands of dollars. Now is a good time to review your I-9 files and process to ensure continued compliance.

Transparency in Coverage mandates and COVID-19 considerations continue to dominate the discussion in the employee benefits compliance space this summer, but an “old faithful” reporting requirement looms soon: the Patient-Centered Outcomes Research Institute (PCORI) filing and fee. The Affordable Care Act imposes this annual per-enrollee fee on insurers and sponsors of self-funded medical plans to fund research into the comparative effectiveness of various medical treatment options.

The typical due date for the PCORI fee is July 31, but because that date falls on a Sunday in 2022, the effective due date is pushed to the next business day, which is Aug. 1.

The filing and payment due by Aug. 1, 2022, is required for policy and plan years that ended during the 2021 calendar year. For plan years that ended Jan. 1, 2021 – Sept. 30, 2021, the fee is $2.66 per covered life. For plan years that ended Oct. 1, 2021 – Dec. 31, 2021 (including calendar year plans that ended Dec. 31, 2021), the fee is calculated at $2.79 per covered life.

Insurers report on and pay the fee for fully insured group medical plans. For self-funded plans, the employer or plan sponsor submits the fee and accompanying paperwork to the IRS. Third-party reporting and payment of the fee (for example, by the self-insured plan sponsor’s third-party claim payor) is not permitted.

An employer that sponsors a self-insured health reimbursement arrangement (HRA) along with a fully insured medical plan must pay PCORI fees based on the number of employees (dependents are not included in this count) participating in the HRA, while the insurer pays the PCORI fee on the individuals (including dependents) covered under the insured plan. Where an employer maintains an HRA along with a self-funded medical plan and both have the same plan year, the employer pays a single PCORI fee based on the number of covered lives in the self-funded medical plan and the HRA is disregarded.

The IRS collects the fee from the insurer or, in the case of self-funded plans, the plan sponsor in the same way many other excise taxes are collected. Although the PCORI fee is paid annually, it is reported (and paid) with the Form 720 filing for the second calendar quarter (the quarter ending June 30). Again, the filing and payment is typically due by July 31 of the year following the last day of the plan year to which the payment relates, but this year the due date pushes to Aug. 1.

IRS regulations provide three options for determining the average number of covered lives: actual count, snapshot and Form 5500 method.

Actual count: The average daily number of covered lives during the plan year. The plan sponsor takes the sum of covered lives on each day of the plan year and divides the number by the days in the plan year.

Snapshot: The sum of the number of covered lives on a single day (or multiple days, at the plan sponsor’s election) within each quarter of the plan year, divided by the number of snapshot days for the year. Here, the sponsor may calculate the actual number of covered lives, or it may take the sum of (i) individuals with self-only coverage, and (ii) the number of enrollees with coverage other than self-only (employee-plus one, employee-plus family, etc.), and multiply by 2.35. Further, final rules allow the dates used in the second, third and fourth calendar quarters to fall within three days of the date used for the first quarter (in order to account for weekends and holidays). The 30th and 31st days of the month are both treated as the last day of the month when determining the corresponding snapshot day in a month that has fewer than 31 days.

Form 5500: If the plan offers family coverage, the sponsor simply reports and pays the fee on the sum of the participants as of the first and last days of the year (recall that dependents are not reflected in the participant count on the Form 5500). There is no averaging. In short, the sponsor is multiplying its participant count by two, to roughly account for covered dependents.

The U.S. Department of Labor says the PCORI fee cannot be paid from ERISA plan assets, except in the case of union-affiliated multiemployer plans. In other words, the PCORI fee must be paid by the plan sponsor; it cannot be paid in whole or part by participant contributions or from a trust holding ERISA plan assets. The PCORI expense should not be included in the plan’s cost when computing the plan’s COBRA premium. The IRS has indicated the fee is, however, a tax-deductible business expense for sponsors of self-funded plans.

Although the DOL’s position relates to ERISA plans, please note the PCORI fee applies to non-ERISA plans as well and to plans to which the ACA’s market reform rules don’t apply, like retiree-only plans.

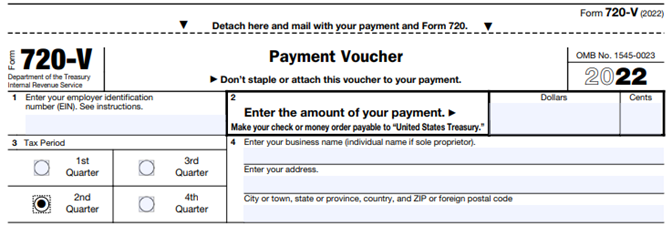

The filing and remittance process to the IRS is straightforward and unchanged from last year. On Page 2 of Form 720, under Part II, the employer designates the average number of covered lives under its “applicable self-insured plan.” As described above, the number of covered lives is multiplied by the applicable per-covered-life rate (depending on when in 2021 the plan year ended) to determine the total fee owed to the IRS.

The Payment Voucher (720-V) should indicate the tax period for the fee is “2nd Quarter.”

Failure to properly designate “2nd Quarter” on the voucher will result in the IRS’ software generating a tardy filing notice, with all the incumbent aggravation on the employer to correct the matter with IRS.

An employer that overlooks reporting and payment of the PCORI fee by its due date should immediately, upon realizing the oversight, file Form 720 and pay the fee (or file a corrected Form 720 to report and pay the fee, if the employer timely filed the form for other reasons but neglected to report and pay the PCORI fee). Remember to use the Form 720 for the appropriate tax year to ensure that the appropriate fee per covered life is noted.

The IRS might levy interest and penalties for a late filing and payment, but it has the authority to waive penalties for good cause. The IRS’s penalties for failure to file or pay are described here.

The IRS has specifically audited employers for PCORI fee payment and filing obligations. Be sure, if you are filing with respect to a self-funded program, to retain documentation establishing how you determined the amount payable and how you calculated the participant count for the applicable plan year.

On April 19, 2022, the Departments of Labor, Health and Human Services, and the Treasury issued additional guidance under the Transparency in Coverage Final Rules issued in 2020. The guidance, FAQs About Affordable Care Act Implementation Part 53, provides a safe harbor for disclosing in-network healthcare costs that cannot be expressed as a dollar amount. They also serve as a timely reminder of the pending July 1, 2022, deadline to begin enforcing the Final Rules.

Background

The Final Rules require non-grandfathered health plans and health insurance issuers to post information about the cost to participants, beneficiaries, and enrollees for in-network and out-of-network healthcare services through machine-readable files posted on a public website. The Final Rules for this requirement are effective for plan years beginning on or after January 1, 2022 (an additional requirement for disclosing information about pharmacy benefits and drug costs is delayed pending further guidance). The Final Rules require that all costs be expressed as a dollar amount. After the Final Rules were published, plans and issuers pointed out that under some alternative reimbursement arrangements in-network costs are calculated as a percentage of billed charges. In those cases, dollar amounts cannot be determined in advance.

FAQ Safe Harbor

The FAQs provide a safe harbor for disclosing costs under a contractual arrangement where the plan or issuer agrees to pay an in-network provider a percentage of billed charges and cannot assign a dollar amount before delivering services. Under this kind of arrangement, they may report the percentage number instead of a dollar amount. The FAQs also provide that where the nature of the contractual arrangement requires the submission of additional information to describe the nature of the negotiated rate, plans and issuers may describe the formula, variables, methodology, or other information necessary to understand the arrangement in an open text field. This is only permitted if the current technical specifications do not support the disclosure via the machine-readable files.

Public Website Requirement

This guidance is pretty narrow and of most interest to plans, issuers, and third-party administrators responsible for the technical aspects of the disclosure. Still, it is a helpful reminder to plan sponsors that the July 1st enforcement deadline for these requirements is rapidly approaching. As a reminder, for fully insured plans the plan sponsor is considered the insurance carrier. However, for self or level funded medical plans the plan sponsor is the employer so they will be the one responsible making sure they are meeting the transparency disclosure requirements. Plans sponsors should remember that these machine-readable files must be posted on a public website. The Final Rules clearly state that the files must be accessible for free, without having to establish a user account, password, or other credentials and without submitting any personal identifying information such as a name, email address, or telephone number. If a third-party website hosts the files, the plan or issuer must post a link to the file’s location on its own public website. Simply posting the files on an individual plan website or the Plan Sponsor’s company intranet falls short of these requirements. Regardless of how a plan opts to comply, The July 1st deadline is right around the corner.

More than 3,300 workers at 70 British companies, ranging from small consultancies to large financial firms, have started working a four-day week with no loss of pay in what organizers of the program call the world’s biggest trial of a shorter workweek.

The pilot program, which launched on June 6 and will run for six months, is organized by the nonprofit 4 Day Week Global, with offices in London and New York City, in partnership with the London-based thinktank Autonomy, the UK’s 4 Day Week Campaign, and researchers at Cambridge University, Oxford University and Boston College.

The researchers will analyze how employees respond to having an extra day off, studying areas such as stress and burnout, job and life satisfaction, health, sleep, energy use and travel.

Joe O’Connor, chief executive of 4 Day Week Global, said the pilot programs puts the UK at the forefront of the four-day week movement. “As we emerge from the pandemic, more and more companies are recognizing that the new frontier for competition is quality of life, and that reduced-hour, output-focused working is the vehicle to give them a competitive edge,” he told The Guardian.

On June 6, O’Connor tweeted, “This is a historic day, as the lives of over 3,000 workers and their families are transformed by the pioneering, forward-thinking approach of their firms to embrace a new approach to how we organize work.”

Shorter Workweek Options

Participating employers in the pilot program agreed to adjust working hours to accord with one of the following options:

4 Day Week Global said it advocates for a “100-80-100” model: 100 percent of pay for workers, who put in 80 percent of their traditional working time, in exchange for maintaining 100 percent of their productivity, according to the group’s website.

Weighing Pros and Cons

The British pilot program follows several other shorter workweek trials in different countries. “Trials by big companies such as Microsoft in Japan and Buffer in the U.S. have shown that a four-day week boosts productivity,” the UK’s 4 Day Week Campaign posted on its website.

“For the next 6 months more than 3,000 UK workers will enjoy the equivalent of a standard bank holiday every single week,” the group tweeted. “And the best thing about it? This could be the future of work for everyone.”

But maybe not. An article in the Harvard Business Review recently pointed out that a study of New Zealand’s move to the four-day workweek found that “not only was work intensified following the change, but so too were managerial pressures around performance measurement, monitoring and productivity,” according to the article’s authors, researchers Emma Russell at the University of Sussex, Caroline Murphy at the University of Limerick and Esme Terry at Leeds University.

“The New Zealand four-day workweek trial rings some alarm bells in that reductions in working days did not necessarily create well-being benefits as workers struggled to meet the demands of their job roles,” the researchers noted. “It is perhaps telling that much of the publicity around the success of Microsoft Japan’s four-day workweek trial rested on how productivity increased substantially during the study period. Employers may need to be careful about promoting outputs over well-being if they want to be seen as investing in their workforce’s work-life balance.”

Still, there is ample evidence that many employees and job candidates would favor the move to a four-day workweek.

Employees Want Flexibility

Ladders, a San Francisco based recruitment firm for executives and professionals, recently surveyed more than 400 job candidates who are active on its search service platform and found that 79 percent said they have already left or would leave a five-day workweek job for a four-day workweek job, provided there is no drop in salary.

“While this strongly indicates an edge in hiring for employers that offer four-day workweeks, nothing is set in stone,” said Ladders CEO Dave Fisch.

The decision to try a shorter workweek should be made after “a careful weighing of the pros and cons for their businesses,” he advised.

However, employers that don’t pursue a shorter workweek may want to “consider other flexible options, or they may find themselves struggling to keep and replace talented people going forward,” Fisch said.

Flexible Schedules as an Alternative Alicia Garcia, chief culture officer at MasterControl, a global technical support company based in Salt Lake City, favors greater flexibility around scheduled hours as an alternative to shorter workweeks. “The biggest issue with a four-day workweek is that it is still rigid,” she said. Whether it is a four- or five-day workweek, “the exact days and times employees are required to work are fixed.” When approached by employees, she said, “the most common request is for ‘flexibility.’ They ask if they can pick up children from school every day and log back in, take an afternoon exercise class, or take a break when the day is feeling stressful. Rarely does the number of hours an employee works surface in these discussions.” She added, “doctor appointments, dentist visits and school performances don’t always fall on the same day of the week.” Garcia advised companies to trust employees to schedule flexibility into their workweek. “Supervisors and managers know if work is getting done and getting done well. They should be empowered to allow flexibility in their teams,” she said. “By developing a culture where managers are trusted to make the best decisions and, in turn, trust their teams to ensure work is covered, companies can develop future senior leaders and recruit the best talent in the market.” |

Citing soaring gas prices, the Internal Revenue Service (IRS) on June 9 announced an increase in the optional standard mileage rate for the final six months of 2022.

Effective July 1 through Dec. 31, 2022, the standard mileage rate for the business use of employees’ vehicles will be 62.5 cents per mile—the highest rate the IRS has ever published—up 4 cents from the 58.5 cents per mile rate effective for the first six months of the year.

The rate is used to compute the deductible costs of operating an automobile for business use, as an alternative to tracking actual costs. Beyond the individual tax deduction, employers often use the standard mileage rate—also called the safe harbor rate—to pay tax-free reimbursements to employees who use their own cars, vans or trucks to conduct business for their employers.

Organizations are typically required to reimburse their workforce for the business use of their mixed-use assets, or personally owned assets such as vehicles that are required for their jobs.

Employers have the option of calculating the actual costs of using their vehicle rather than using the standard mileage rates.

The IRS normally updates standard mileage rates once a year in the fall for the next calendar year. For vehicle use from Jan. 1 through June 30, 2022, employers and employees should use the rates set forth in IRS Notice 2022-03.

While fuel costs are a significant factor in the mileage figure, other items enter into the calculation of mileage rates, such as depreciation and insurance and other fixed and variable costs, the IRS noted. For cars employees use for business, the portion of the standard mileage rate treated as depreciation will stay at 26 cents per mile for 2022.

Midyear increases in the optional mileage rates are rare. The last time the IRS made such an increase was in 2011.

In a surprise move, federal immigration officials recently announced that they will permit remote review of new hires’ I-9 documentation for those who work exclusively in a remote setting due to COVID-19 related precautions through October 31, 2022. According to the April 25th announcement, U.S. Immigration and Customs Enforcement (ICE) has said that the requirement that employers inspect employees’ Form I-9 identity and employment eligibility documentation in-person applies only to those employees who physically report to work at a company location on any regular, consistent, or predictable basis for at least the next six months. Could this continued flexibility be a welcome sign of things to come?

(more…)