Healthcare Reform continues to roll on despite all of its opponents. While 2014 brought the implementation of the health insurance exchanges, the Individual Mandate, and a host of new rules relating to employer-provided health coverage, 2015 marks the start of yet another major component of the Affordable Care Act (ACA): the Employer Mandate.

In the a recent article written by Fisher & Phillips LLP attorney Steven Witt, he discusses the potential risks employers can face if they are not careful in how they implement (and document) their compliance strategies with regards to the Employer Mandate.

The Employer Mandate requires large employers to offer compliant group health coverage to their “full-time employees” and their dependents or face excise tax penalties. Say you are a large employer who has never offered health insurance (or perhaps only to a small subset of your employees). You do not want to bankrupt the company and offer health insurance to your entire workforce, nor do you want to face tax penalties. Instead, you opt for what the Employer Mandate calls for: you offer health insurance coverage to only your full-time employees.

If you decide to only offer coverage to your “full-time” employees, simply setting measurement period dates with your human resources department and running payroll reports to determine who is “full-time” will not sufficiently limit the risk of controversy and potential legal liability. You will be much better off to clearly define these eligibility rules in writing and make sure any old, conflicting eligibility rules are updated.

Leaving existing plan documents and other materials (e.g., employee handbooks) to define health insurance eligibility with something vague like “full-time employees: employees who regularly work 30 or more hours per week,” is only inviting trouble. You will no doubt have employees (with attorneys) who could make plausible arguments that they “regularly” work 30 or more hours a week and can point to your existing written documents as evidence they should have been offered health insurance. Without clearly setting out new eligibility rules, it will be a much steeper uphill battle for the employer to defend itself.

On the other hand, if such employees attempt to claim that they were unfairly denied health insurance coverage, an employer should be on much stronger footing to defend its position that those employees are not “full-time” if it can point to written documentation outlining items such as (a) date ranges used for measurement periods and stability periods; (b) waiting periods for newly-eligible employees; and © how to treat employees in special circumstances, such as those who are promoted from a part-time position to a full-time position, those on a leave of absence, or rehired employees.

If you have not already done this, it is not too late. Even employers subject to the Employer Mandate in 2015 can still timely revise their SPDs or perhaps draft stand-alone benefits eligibility documents or other “wrap” documents to fully outline new eligibility rules. Steven advises employers to pay close attention as additional regulations and agency guidance continues to roll out to ensure they stay in compliance with ERISA, the ACA, and other related federal and state health insurance-related laws.

Form 1095-A is a tax form that will be sent to consumers who have been enrolled in health insurance through the Marketplace in the past year. Just like employees receive a W-2 from their employer, consumer who had a plans on the Marketplace will also receive form 1095-A from the Marketplace, which they will need for taxes. Similar to how households receive multiple W-2s if individuals have multiple jobs, some households will get multiple Form 1095-As if they were covered under different plans or changed plans during the year. The 1095-A forms will be mailed direct to consumer’s last known home address provided to the Marketplace and will be postmarked by February 2, 2015.

Form 1095-A provides information to consumers that is needed to complete Form 8962, Premium Tax Credit (PTC). The Marketplace has also reporting this information to the IRS. Consumers will file Form 8962 with their tax returns if they want to claim the premium tax credit or if they received premium assistance through advance credit payments made to their insurance provider.

Beginning January 1, 2015, employers have new reporting obligations for health plan coverage, to allow the government to administer the “pay or play” penalties to be assessed against employers that do not offer compliant coverage to their full-time employees.

Even though the penalties only apply if there are 100 or more employees for 2015, employers with 50 or more full-time equivalent employees are required to report for 2015. Also, note this reporting is required even if the employer does not maintain any health plan.

Employers that provide self-funded group health coverage also have reporting obligations, to allow the government to administer the “individual mandate” which results in a tax on individuals who do not maintain health coverage.

These reporting obligations will be difficult for most employers to implement. Penalties for non-compliance are high, so employers need to begin now with developing a plan on how they will track and file the required information.

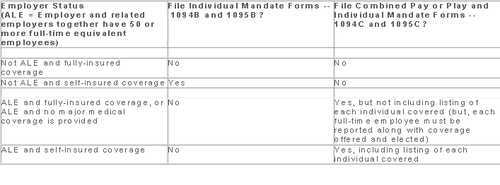

Pay or Play Reporting. Applicable large employers (ALEs) must report health coverage offered to employees for each month of 2015 in an annual information return due early in 2016. ALEs are employers with 50 or more full-time equivalent (FTE) employees. Employees who average 30 hours are counted as one, and those who average less than 30 hours are combined into an equivalent number of 30 hour employees to determine if there are 50 or more FTE employees. All employees of controlled group, or 80% commonly owned employers, are also combined to determine if the 50 FTE threshold is met.

Individual Mandate Reporting. Self-funded employers, including both ALEs and small employers that are not ALEs, must report each individual covered for each month of the calendar year. For fully-insured coverage, the insurance carrier must report individual month by month coverage. The individual mandate reporting is due early in 2016 for each month of 2015.

Which Form? ALE employers have one set of forms to report both the pay or play and the individual mandate information – Forms 1094C and 1095C. Insurers and self-insured employers that are not ALEs use Forms 1094B and 1095B to report the individual mandate information. Information about employee and individual coverage provided on these forms must also be reported by the employer to its employees as well as to COBRA and retiree participants. Forms 1095B and 1095C can be used to provide this information, or employers can provide the information in a different format.

The following chart summaries which returns are filed by employers:

Who Reports? While ALE status is determined on a controlled group basis, each ALE must file separate reports. Employers will need to provide insurance carriers, and third party administrators who process claims for self-funded coverage (if they will assist the employer with reporting), accurate data on the employer for whom each covered employee works. If an employee works for more than one ALE in a controlled group, the employer for whom the highest number of hours is worked does the reporting for that employee.

Due Date for Filing. The due date of the forms matches the due dates of Forms W-2, and employers may provide the required employee statements along with the W-2. Employee reporting is due January 31st and reporting to the IRS is due each February 28th, although the date is extended until March 31st if the forms are filed electronically. If the employer files 250 or more returns, the returns must be filed electronically. Reporting to employees can only be made electronically if the employee has specifically consented to receiving these reports electronically.

Penalties. Failure to file penalties can total $200 per individual for whom information must be reported, subject to a maximum of $3 million per year. Penalties will not be assessed for employers who make a good faith effort to file correct returns for 2015.

What Information is Required? For the pay or play reporting, each ALE must file a Form 1094C reporting the number of its full-time employees (averaging 30 hours) and total employees for each calendar month, whether the ALE is in a “aggregated” (controlled) group, a listing of the name and EIN of the top 30 other entities in the controlled group (ranked by number of full-time employees), and any special transition rules being used for pay or play penalties. ALE’s must also file a 1095C for each employee who was a full-time employee during any calendar month of the year. The 1095C includes the employee’s name, address and SSN, and month by month reporting of whether coverage was offered to the employee, spouse and dependents, the lowest premium for employee only coverage, and identification of the safe-harbor used to determine affordability. This information is used to determine pay or play penalty taxes and to verify the individuals’ eligibility for subsidies toward coverage costs on the Federal and state exchanges.

If the ALE provides self-funded coverage, the ALE must also report on the 1095C the name and SSN of each individual provided coverage for each calendar month. If an employer is not an ALE, but is self-funded, the name and SSN of each covered individual is reported on the 1095B and the 1094B is used to transmit the forms 1095B to the IRS.

A chart is available that sets out what data must be reported on each form, to help employers determine what information they need to track. Click here to access the chart.

Next Steps. Employers will need to determine how much help their insurance carrier or TPA can provide with the reporting, and then the employer’s HR, payroll and IT functions will need to work together to be sure the necessary information is being tracked and can be produced for reporting in January 2016.

Members of the U.S. House of Representatives voted on January 8, 2015 to redefine full-time employment under the Affordable Care Act (ACA) to employees who work at least 40 hours a week rather than 30 hours a week.

The Save American Workers Act, passed the House with a vote of 252-172 with full Republican support and 12 Democratic voters. The legislation would amend the Internal Revenue Code by changing the definition of full-time employee to cover individuals who work, on average, at least 40 hours per week for purposes of the employer mandate to provide minimum essential health care coverage under the ACA.

Despite the bill’s passage in the House, the fate of the bill in the U.S. Senate remains uncertain. In addition, Republicans have not garnered enough support to override the veto promised by President Obama if the bill did pass Congress.

According to Politico, “The House has cleared more than 50 assorted measures to repeal or roll back Obamacare, but this is the first time the House can propel legislation to a GOP-controlled Senate, potentially forcing President Barack Obama to either accept changes to his signature domestic achievement or use his veto power.”

Some supporters of the change, including the U.S. Chamber of Commerce, argue that the current standard deviates from the widely accepted definition of full-time work. It is argued that it provides an incentive for employers to reduce hours, particularly for low-wage workers, to avoid offering healthcare coverage.

This month, employers with 100 or more employees will be required to offer health insurance to at least 70% of employees who works at least 30 hours a week or else pay a penalty.

The NY Times comments:

By adjusting that threshold to 40 hours, Republicans — strongly backed by a number of business groups — said that they would re-establish the traditional 40-hour workweek and prevent businesses cutting costs from radically trimming worker hours to avoid mandatory insurance coverage. They contend that the most vulnerable workers are low-skilled and underpaid, working 30 to 35 hours a week, and now facing cuts to 29 hours or less so their employers do not have to insure them. With passage of the law, those workers would not have to get employer-sponsored health care, and their workweek would remain intact.

Analysis by the Congressional Budget Office found that the bill would increase the U.S. deficit by $53 billion over the course of a decade because fewer employers would pay penalties and one million employees would not have coverage through their job. Democrats cite these reasons as evidence that the bill is simply an attempt to dismantle the ACA.

A central issue of this bill is how far employers would go to avoid mandated coverage. A majority of employees already work 40 hours a week rather than 30. That being said, few employers would cut worker hours from 40 to 29, but many would be willing to cut hours from 40 to 39, the New York Times ventures, “That means raising the definition of a full-time worker under the health care law would put far more workers at risk.”

As 2015 begins, the Occupational Safety and Health Administration (OSHA) is sharpening its emphasis on inspecting and citing employers who violate its recordkeeping standard. This takes on greater importance because of the changes and new reporting requirements effective on January 1, 2015.

New OSHA Reporting Rules

Under the new rules, all employers are now required to contact OSHA within 24 hours following an occurrence of any in-patient hospitalizations, amputations, or loss of an eye, as well as the current requirement to contact OSHA within eight hours following a fatality. For reporting compliance, employers have three options when contacting OSHA: 1) call the nearest area office; 2) call OSHA’s 24-hour hotline 1-800-321-OSHA(6742); or 3) report online.

New Recordkeeping And Posting Requirements

Many new categories of employers must now maintain and post OSHA injury and illness records going forward. Employers who were already covered must complete and post their 2014 annual summary by February 1, 2015 and keep it posted until April 30, 2015. Employers must utilize the annual summary form (form 300A) to comply with the posting requirements. Even if you have no recordable injury or illness, you must still complete your 300 logs and post the 300A summary.

Below are some key details that are frequently misunderstood or overlooked which can lead to OSHA citations.

Executive Certification

OSHA’s recordkeeping standard requires a certification of the 300A summary by a company executive. Four specific management officials may be considered “company executives” for purposes of certifying the 300A summary: 1) an owner of the company; 2) an officer of the corporation; 3) the highest-ranking company official working at the location; or 4) the immediate supervisor of the highest-ranking company official working at the location. This official must certify that he or she has reviewed the OSHA 300 logs and related records, and reasonably believes, based on knowledge of the process underlying the development of the data, that the posted summary is accurate and complete.

OSHA describes this requirement as imposing “senior management accountability” for the integrity and accuracy of the reported data. Human resources managers and safety directors normally cannot sign the OSHA 300A summary unless they are officers of the company.

Number Of Employees And Hours Worked

The annual summary requires employers to include a calculation of the annual average number of employees covered by the log and the total hours worked by all covered employees. The purpose of this requirement is to help employers compare the relative frequency of significant occupational injuries and illnesses at their workplace as compared to other establishments.

Posting Process

The 300A summary must be posted in each establishment in a conspicuous place or places where notices to employees are customarily posted. You are under a duty to ensure that the posted annual summary is not altered, defaced or obscured during the entire posting period.

Those employers who maintain these records in electronic form should still retain the signed posted summary after the February 1 to April 30 posting period, to prove that it was properly signed.

You should provide copies of the 300A summary to any employee who may not see the posted summary because they do not report to a fixed location on a regular basis. Even where an establishment has had no recordable injuries or illnesses, you must still post the 300A summary with zeros in the appropriate lines and certified by a company executive.

Record Review

Before the annual summary is prepared, the recordkeeping rule imposes an express duty to review the log (form 300) to verify that entries are complete and accurate. Employers must review the records as “extensively as necessary” to ensure accuracy.

OSHA scrutinizes the forms 301, 300 and 300A for even minor errors in descriptions and boxes checked. Take time to review the forms for technical errors as well as to review accident reports, first aid logs and other related materials to ensure that all recordable incidents have been included and that records are consistent. Employers have a duty to update and maintain records for five years plus the current year and provide them upon request for inspection by OSHA investigators.

Newly Covered Employers

Finally, all employers who have previously been partially exempt from OSHA recordkeeping requirements and were not required to maintain the form 300, should review the updated industry exemption list to see if they are now covered. Under the new rule, 25 industries that were previously exempt are not, and must now maintain the OSHA 300 logs and other required documentations.

On December 22, 2014, the Departments of Health and Human Services (HHS) issued proposed regulations for changes to the Summary of Benefits and Coverage (SBC).

The proposed regulations clarify when and how a plan administrator or insurer must provide an SBC, shortens the SBC template, adds a third cost example, and revises the uniform glossary. The proposed regulations provide new information and also incorporate several FAQs that have been issued since the final SBC regulations were issued in 2012.

These proposed changes are effective for plan years and open enrollment period beginning on or after September 1, 2015. Comments on the proposed regulations will be accepted until March 2,2015 and are encourages on many of the provisions.

New Template

The new SBC template eliminates a significant amount of information that the Departments characterized as not being required by law and/or as having been identified by consumer testing as less useful for choosing coverage.

The sample completed SBC template for a standard group health plan has been reduced from four double-sided pages to two-and-a-half double-sided pages. Some of the other changes include:

Glossary Revisions

Revisions to the uniform glossary have also been proposed. The glossary must be available to plan participants upon request. Some definitions have been changed and new medical terms such as claim, screening, referral and specialty drug have been added. Additional terms related to health care reform such as individual responsibility requirement, minimum value and cost-sharing reductions have also been added.

Paper vs Electronic Distribution

SBCs may continue to be provided electronically to group plan participants in connection with their online enrollment or online renewal of coverage. SBCs may also be provided electronically to participants who request an SBC online. These individuals must also have the option to receive a paper copy upon request.

SBCs for self-insured non-federal government plans may continue to be provided electronically if the plan conforms to either the electronic distribution requirements that apply ERISA plan or the rules that apply to individual health insurance coverage.

Types of Plans to Which SBCs Apply

The regulations confirm that SBCs are not required for expatriate health plans, Medicare Advantage plans or plans that qualify as excepted benefits. Excepted benefits include:

SBCs are required for:

Florida’s minimum wage is currently $7.93 per hour. Beginning January 1, 2015, Florida’s minimum wage will increase to $8.05 per hour, which is a 1.5% (or $0.12) increase from last year.

Employers of “tipped employees” who meet eligibility requirements for the tip credit under the Fair Labor Standards Act (FLSA) may count tips actually received as wages under the FLSA. The employer, however, must pay “tipped employees” a direct wage. Effective January 1, 2015, the new minimum wage for tipped employees should become $5.03 per hour plus tips.

Florida law requires a new minimum wage calculation each year on September 30, based on the Consumer Price Index. If that calculation is higher than the federal rate (which is currently $7.25 per hour), the state’s rate would take effect the following January.

Please contact our office if you need a copy of the 2015 Florida Minimum Wage Poster. Be sure to post the new Minimum Wage Poster by January 1st.

The Affordable Care Act will require Applicable Large Employers (i.e. large employers subject to the employer mandate) and employers sponsoring self-insured plans to comply with new annual IRS reporting requirements. The first reporting deadline will be February 28, 2016 as to the data employers collect during the 2015 calendar year. The reporting provides the IRS with information it needs to enforce the Individual Mandate (i.e. individuals are penalized for not having health coverage) and the Employer Mandate (i.e. large employers are penalized for not offering health coverage to full-time employees). The IRS will also require employers who offer self-insured plans to report on covered individuals.

Large employers and coverage providers must also provide a written statement to each employee or responsible individual (i.e. one who enrolls one or more individuals) identifying the reported information. The written statement can be a copy of the Form.

The IRS recently released draft Forms 1094-C and 1095-C and draft Forms 1094-B and 1095-B, along with draft instructions for each form.

Which Forms Do I File?

When?

Statements to employees and responsible individuals are due annually by January 31. The first statements are due January 31, 2016.

Forms 1094-B, 1095-B, 1094-C and 1095-C are due annually by February 28 (or by March 31, if filing electronically). The first filing is due by February 28, 2016 (or March 31, 2016, if filing electronically).

Even though the forms are not due until 2016, the annual reporting will be based on data from the prior year. Employers need to plan ahead now to collect data for 2015. Many employers have adopted the Look Back Measurement Method Safe Harbor (“Safe Harbor”) to identify full-time employees under the ACA. The Safe Harbor allows employers to “look back” on the hours of service of its employees during 2014 or another measurement period. There are specific legal restrictions regarding the timing and length of the periods under the Safe Harbor, so employers cannot just pick random dates. Employers also must follow various rules to calculate hours of service under the Safe Harbor. The hours of service during the measurement period (which is likely to include most of 2014) will determine whether a particular employee is full-time under the ACA during the 2015 stability period. The stability period is the time during which the status of the employee, as full-time or non-full-time, is locked in. In 2016, employers must report their employees’ full-time status during the calendar year of 2015. Therefore, even though the IRS forms are not due until 2016, an employee’s hours of service in 2014 will determine how an employer reports that employee during each month of 2015. Employers who have not adopted the Safe Harbor should consider doing so because it allows an employer to average hours of service over a 12-month period to determine the full-time status of an employee. If an employer does not adopt the Safe Harbor, the IRS will require the employer to make a monthly determination, which is likely to increase an employer’s potential exposure to penalties.

What Must the Employer Report?

Form 1095-C

There are three parts to Form 1095-C. An applicable large employer must file one Form 1095-C for each full-time employee. If the applicable large employer sponsors self-insured health plans, it must also file Form 1095-C for any employee who enrolls in coverage regardless of the full-time status of that employee.

Form 1095-C requires the employer to identify the type of health coverage offered to a full-time employee for each calendar month, including whether that coverage offered minimum value and was affordable for that employee. Employers must use a code to identify the type of health coverage offered and applicable transition relief.

Employers that offer self-insured health plans also must report information about each individual enrolled in the self-insured health plan, including any full-time employee, non-full-time employee, employee family members, and others.

Form 1094-C

Applicable large employers use Form 1094-C as a transmittal to report employer summary information and transmit its Forms 1095-C to the IRS. Form 1094-C requires employers to enter the name and contact information of the employer and the total number of Forms 1095-C it submits. It also requires information about whether the employer offered minimum essential coverage under an eligible employer-sponsored plan to at least 95% of its full-time employees and their dependents for the entire calendar year, the number of full-time employees for each month, and the total number of employees (full-time or non-full-time) for each month.

Form 1095-B

Employers offering self-insured coverage use Form 1095-B to report information to the IRS about individuals who are covered by minimum essential coverage and therefore are not liable for the individual shared responsibility payment. These employers must file a Form 1095-B for eachindividual who was covered for any part of the calendar year. The employer must make reasonable efforts to collect social security numbers for covered individuals.

Form 1094-B

Employers who file Form 1095-B will use Form 1094-B as a transmittal form. It asks for the name of the employer, the employer’s EIN, and the name, telephone number, and address of the employer’s contact person.

Failure to Report – What Happens?

The IRS will impose penalties for failure to timely provide correct written statements to employees. The IRS will also impose penalties for failure to timely file a correct return. For the 2016 reporting on 2015 data, the IRS will not impose a penalty for good faith compliance. However, the IRS specified that good faith compliance requires that employers provide the statements and file the returns.

On November 7th, 2014, the U.S. Supreme Court agreed to hear King v. Burwell. The case will argue whether or not subsidies in the marketplace should be limited to states with state-run Exchanges. According to the New York Times, “If the challengers are right, millions of people receiving subsidies (through the federal Exchange) would become ineligible for them, destabilizing and perhaps dooming the law.” Arguments are due to begin in December, and a ruling will be issue by next June.

The key question in the case deals with the conflicting IRS ruling stating that “subsidies are allowed whether the exchange is run by a state or by the federal government.” Those challenging the law in this case say that this rule conflicts with the statutory language set forth in the Affordable Care Act (ACA).

Two lower courts, the U.S. Court of Appeals for the District of Columbia in Halbig v. Burwell and the U.S. Court of Appeals for the Fourth Circuit in King v. Burwell, have already issued conflicting opinions regarding the IRS’ authority to administer subsidies in federally facilitated Exchanges. In addition, two other cases are being litigated in the lower courts on the same issue. In Pruitt v. Burwell, a district court in Oklahoma ruled against the IRS in September, and a decision in a fourth court case, Indiana v. IRS, is expected shortly. Of course, the Supreme Court ruling could render the lower court decisions moot.

The Department of Labor has just published a series of FAQs regarding premium reimbursement arrangements. Specifically, the FAQs address the following arrangements:

Situation #1: An arrangement in which an employer offers an employee cash to reimburse the purchase of an individual market policy.

When an employer provides cash reimbursement to the employee to purchase an individual medical policy, the DOL takes the position that the employer’s payment arrangement is part of a plan, fund, or other arrangement established or maintained for the purpose of providing medical care to employees, regardless of whether the employer treats the money as pre or post tax to the employee. Therefore, the arrangement is considered a group health plan that is subject to the market reform provisions of the Affordable Care Act applicable to group health plans and because it does not comply (and cannot comply) with such provisions, it may be subject to penalties.

Situation #2: An arrangement in which an employer offers employees with high cost claims a choice between enrollment in its group health plan or cash.

The DOL takes the position that offering a choice between enrolling in the group health plan or cash only to employees with a high claims risk would be discriminatory based on one or more health factors. The DOL states that such arrangements will violate such nondiscrimination provisions regardless of whether (1) the cash payment is treated by the employer as pre-tax or post-tax to the employee, (2) the employer is involved in the selection or purchase of any individual medical policy, or (3) the employee obtains any individual health insurance. The DOL also notes that such an arrangement, depending on facts and circumstances, could result in discrimination under an employer’s cafeteria plan.

Situation #3: An arrangement where an employer cancels its group policy, sets up a reimbursement plan (like an HRA) that works with health insurance brokers or agents to help employees select individual insurance policies, and allows eligible employees to access the premium tax credits for Marketplace coverage.

The DOL takes the position that such an arrangement is a considered a group health plan and, therefore, employees participating in such arrangement are ineligible for premium tax credits (or cost-sharing reductions) for Marketplace coverage. The DOL also takes the position that such arrangements are subject to the market reform provisions of the ACA and cannot be integrated with individual market policies to satisfy the market reforms. Thus, such arrangements can trigger penalties.

Key Takeaway

There has been quite a bit of banter regarding whether any of the foregoing arrangements could be an effective way for employers to avoid complying with the market reforms and other provisions of the Affordable Care Act applicable to group health plans. These FAQs are a strong indication that the DOL will be forceful in its interpretation and enforcement of these provisions.